-

首页

-

教学项目展开 / 收起

sidenav background教学项目

sidenav header background计量经济学一班—2010年春季学期双学位课程介绍

发布日期:2010-03-01 12:28

2010年 北京大学国家发展研究院 双学位计量经济学一班

课程简介: 学习基础的计量经济原理

上课地点: 理教117

上课时间:星期一:11-12节(19:10-21:00); 星期六:7-8节(14:40-16:30)

实习课: 星期六:9-10节(16:50-18:40), 理教117.

指定教材: Stock, James and Mark Watson: Introduction to Econometrics. Shanghai University of Finance &Economics Press.

考核标准: 平时成绩(30%),期中考(30%),期末考(40%)

课程规则:

1 Generally, this course is NOT graded by curve. Transparent grading policy is upheld.

2 Copying homework and cheating in the exam are strictly prohibited. Any violation will be reported to the university. (严格规定不得有作业抄袭与考试作弊的情事. 违反者将移送校方按校规处理).

3 No make-up exam except for medical emergency. Research field trip, taking GRE or TOFEL etc. is NOT a legitimate excuse.

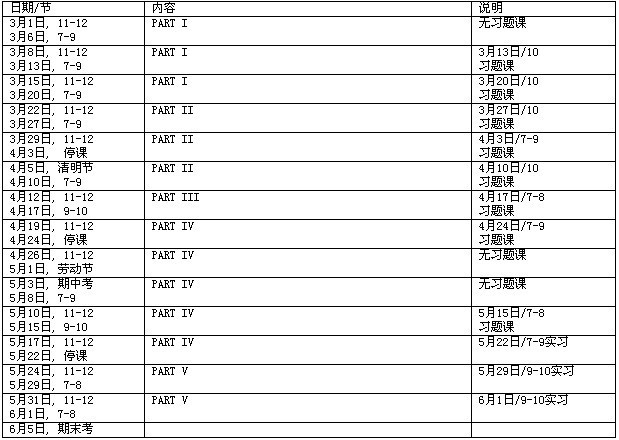

教学计划

教学内容:

Part I Linear Regression with One Regressor (Chapter 4 and 15)

(a) Model specification, estimation and Goodness of fit. (4-1,4-2, 4-8)

(b) Assumptions and Gauss-Markov Theorem (4-3, 15-5)

(c) Sampling distribution and Interval estimation (4-4, 4-6)

(d) Statistical Inference: t test. (4-5, 15-4)

(e) Consistency and Asymptotic normality (15-1, 15-2, 15-3)

(f) Heteroskedasticity and Weighted least squares. (4-9, 15-6)

Part II Linear Regression with Multiple Regressors (Chapter 5 and 16)

(a) OLS and LS assumptions (5-3,5-4, 16-1)

(b) Sampling distribution of OLS (5-5,16-2)

(c) Test for individual coefficients (5-6, 16-4)

(d) Tests of Joint Hypothesis (5-7, 5-8, 16-4)

(e) GLS and HSK-robust standard errors (16-2, 16-6)

(f) Omitted Variable Bias (5.1,5.11)

(g) Threats to internal validity (7.1, 7.2)

Part III Nonlinear Regression Function

(a) Log linear models (6-2)

(b) Polynomials (6.1, 6.2)

(c) Dummy variable and Interaction terms (6-3)

(d) Specification errors.

Part IV Time Series Regression

(a) Autoregressions (12-3)

(b) Autoregressive distributed lag Model (12-4, 12.5)

(c) Nonstationary Time series: Stochastic Trend and Unit root test (12-6)

(d) Nonstationary Time series: Breaks (12.7)

Part V Dynamic Causal Effects

(a) Causal effects and Erogeneity (13.2)

(b) Estimation with distributed lag Model (13-3)

(c) HAC standard errors (13-4)

(d) Estimation with strictly exogenous variables (13.5).

Remark:

Review of Chapter 2 is strongly suggested.

国家发展研究院官方微信

Copyright© 1994-2012 北京大学 国家发展研究院 版权所有, 京ICP备05065075号-1

保留所有权利,不经允许请勿挪用

-

首页

-

教学项目展开 / 收起

sidenav background教学项目

sidenav header background计量经济学一班—2010年春季学期双学位课程介绍

发布日期:2010-03-01 12:28

2010年 北京大学国家发展研究院 双学位计量经济学一班

课程简介: 学习基础的计量经济原理

上课地点: 理教117

上课时间:星期一:11-12节(19:10-21:00); 星期六:7-8节(14:40-16:30)

实习课: 星期六:9-10节(16:50-18:40), 理教117.

指定教材: Stock, James and Mark Watson: Introduction to Econometrics. Shanghai University of Finance &Economics Press.

考核标准: 平时成绩(30%),期中考(30%),期末考(40%)

课程规则:

1 Generally, this course is NOT graded by curve. Transparent grading policy is upheld.

2 Copying homework and cheating in the exam are strictly prohibited. Any violation will be reported to the university. (严格规定不得有作业抄袭与考试作弊的情事. 违反者将移送校方按校规处理).

3 No make-up exam except for medical emergency. Research field trip, taking GRE or TOFEL etc. is NOT a legitimate excuse.

教学计划

教学内容:

Part I Linear Regression with One Regressor (Chapter 4 and 15)

(a) Model specification, estimation and Goodness of fit. (4-1,4-2, 4-8)

(b) Assumptions and Gauss-Markov Theorem (4-3, 15-5)

(c) Sampling distribution and Interval estimation (4-4, 4-6)

(d) Statistical Inference: t test. (4-5, 15-4)

(e) Consistency and Asymptotic normality (15-1, 15-2, 15-3)

(f) Heteroskedasticity and Weighted least squares. (4-9, 15-6)

Part II Linear Regression with Multiple Regressors (Chapter 5 and 16)

(a) OLS and LS assumptions (5-3,5-4, 16-1)

(b) Sampling distribution of OLS (5-5,16-2)

(c) Test for individual coefficients (5-6, 16-4)

(d) Tests of Joint Hypothesis (5-7, 5-8, 16-4)

(e) GLS and HSK-robust standard errors (16-2, 16-6)

(f) Omitted Variable Bias (5.1,5.11)

(g) Threats to internal validity (7.1, 7.2)

Part III Nonlinear Regression Function

(a) Log linear models (6-2)

(b) Polynomials (6.1, 6.2)

(c) Dummy variable and Interaction terms (6-3)

(d) Specification errors.

Part IV Time Series Regression

(a) Autoregressions (12-3)

(b) Autoregressive distributed lag Model (12-4, 12.5)

(c) Nonstationary Time series: Stochastic Trend and Unit root test (12-6)

(d) Nonstationary Time series: Breaks (12.7)

Part V Dynamic Causal Effects

(a) Causal effects and Erogeneity (13.2)

(b) Estimation with distributed lag Model (13-3)

(c) HAC standard errors (13-4)

(d) Estimation with strictly exogenous variables (13.5).

Remark:

Review of Chapter 2 is strongly suggested.